'%20stroke-width='15'%20stroke-linecap='round'%20stroke-dasharray='0%2044%200%2044%200%2044%200%2044%200%20360'%20cx='100'%20cy='100'%20r='70'%20transform-origin='center'%3e%3canimateTransform%20type='rotate'%20attributeName='transform'%20calcMode='discrete'%20dur='2'%20values='360;324;288;252;216;180;144;108;72;36'%20repeatCount='indefinite'%3e%3c/animateTransform%3e%3c/circle%3e%3c/svg%3e%20--%3e%3csvg%20width='78'%20height='78'%20viewBox='0%200%2078%2078'%20fill='none'%20xmlns='http://www.w3.org/2000/svg'%3e%3crect%20x='14'%20y='17'%20width='48'%20height='44'%20fill='white'%20/%3e%3cpath%20d='M24.0741%2034.9365C21.432%2034.9365%2019.377%2037.0503%2019.377%2039.7365C19.377%2042.4228%2021.4466%2044.5512%2024.0741%2044.5512C26.7016%2044.5512%2028.7714%2042.4375%2028.7714%2039.7365C28.7714%2037.0356%2026.7016%2034.9365%2024.0741%2034.9365Z'%20fill='%235082AF'%20/%3e%3cpath%20d='M38.5614%200C17.2624%200%200%2017.2624%200%2038.5616C0%2059.8606%2017.2624%2077.123%2038.5614%2077.123C59.8606%2077.123%2077.123%2059.8606%2077.123%2038.5616C77.123%2017.2624%2059.8606%200%2038.5614%200ZM32.1469%2047.5597H28.7707V46.0624L28.6533%2046.1651C27.2734%2047.2661%2025.644%2047.8386%2023.8093%2047.8386C19.3469%2047.8386%2015.9853%2044.3597%2015.9853%2039.7506C15.9853%2035.1413%2019.3469%2031.6624%2023.8093%2031.6624C25.5853%2031.6624%2027.2734%2032.2349%2028.6533%2033.3358L28.7707%2033.4238V31.9267H32.1469V47.5597ZM43.0238%2044.5506C44.7707%2044.5506%2046.3413%2043.611%2047.1486%2042.0992H50.7891C49.7616%2045.5781%2046.723%2047.824%2043.0238%2047.824C38.4147%2047.824%2034.9358%2044.345%2034.9358%2039.7358C34.9358%2035.1267%2038.4147%2031.6477%2043.0238%2031.6477C46.7083%2031.6477%2049.7469%2033.8936%2050.7891%2037.3872H47.1634C46.356%2035.8459%2044.8147%2034.9211%2043.0093%2034.9211C40.367%2034.9211%2038.312%2037.0349%2038.312%2039.7358C38.312%2042.4368%2040.3818%2044.5506%2043.0093%2044.5506H43.0238ZM60.213%2035.2H56.9835V42.7157C56.9835%2043.5963%2057.6882%2044.2862%2058.5835%2044.2862H60.213V47.5597H58.5835C55.7506%2047.5597%2053.6074%2045.4754%2053.6074%2042.7157V29.2992H56.9835V31.9267H60.213V35.2Z'%20fill='%235082AF'%20/%3e%3c/svg%3e)

'%3e%3cpath%20d='M24.0741%2034.937C21.432%2034.937%2019.377%2037.0508%2019.377%2039.737C19.377%2042.4233%2021.4466%2044.5517%2024.0741%2044.5517C26.7016%2044.5517%2028.7714%2042.438%2028.7714%2039.737C28.7714%2037.0361%2026.7016%2034.937%2024.0741%2034.937Z'%20fill='%235082AF'/%3e%3cpath%20d='M38.5614%200C17.2624%200%200%2017.2624%200%2038.5616C0%2059.8606%2017.2624%2077.123%2038.5614%2077.123C59.8606%2077.123%2077.123%2059.8606%2077.123%2038.5616C77.123%2017.2624%2059.8606%200%2038.5614%200ZM32.1469%2047.5597H28.7707V46.0624L28.6533%2046.1651C27.2734%2047.2661%2025.644%2047.8386%2023.8093%2047.8386C19.3469%2047.8386%2015.9853%2044.3597%2015.9853%2039.7506C15.9853%2035.1413%2019.3469%2031.6624%2023.8093%2031.6624C25.5853%2031.6624%2027.2734%2032.2349%2028.6533%2033.3358L28.7707%2033.4238V31.9267H32.1469V47.5597ZM43.0238%2044.5506C44.7707%2044.5506%2046.3413%2043.611%2047.1486%2042.0992H50.7891C49.7616%2045.5781%2046.723%2047.824%2043.0238%2047.824C38.4147%2047.824%2034.9358%2044.345%2034.9358%2039.7358C34.9358%2035.1267%2038.4147%2031.6477%2043.0238%2031.6477C46.7083%2031.6477%2049.7469%2033.8936%2050.7891%2037.3872H47.1634C46.356%2035.8459%2044.8147%2034.9211%2043.0093%2034.9211C40.367%2034.9211%2038.312%2037.0349%2038.312%2039.7358C38.312%2042.4368%2040.3818%2044.5506%2043.0093%2044.5506H43.0238ZM60.213%2035.2H56.9835V42.7157C56.9835%2043.5963%2057.6882%2044.2862%2058.5835%2044.2862H60.213V47.5597H58.5835C55.7506%2047.5597%2053.6074%2045.4754%2053.6074%2042.7157V29.2992H56.9835V31.9267H60.213V35.2Z'%20fill='%235082AF'/%3e%3cpath%20d='M160%2026.3203H156.463V47.4579H160V26.3203Z'%20fill='%235082AF'/%3e%3cpath%20d='M149.946%2033.0427C148.595%2031.9859%20146.907%2031.3547%20145.028%2031.3547C140.536%2031.3547%20137.102%2034.8923%20137.102%2039.5456C137.102%2044.1987%20140.536%2047.7363%20145.028%2047.7363C146.907%2047.7363%20148.595%2047.1051%20149.946%2046.0483V47.4722H153.483V31.6189H149.946V33.0427ZM145.292%2044.2869C142.65%2044.2869%20140.639%2042.2319%20140.639%2039.5309C140.639%2036.8299%20142.65%2034.7749%20145.292%2034.7749C147.935%2034.7749%20149.946%2036.8299%20149.946%2039.5309C149.946%2042.2319%20147.935%2044.2869%20145.292%2044.2869Z'%20fill='%235082AF'/%3e%3cpath%20d='M131.642%2033.0427C130.291%2031.9859%20128.603%2031.3547%20126.725%2031.3547C122.233%2031.3547%20118.798%2034.8923%20118.798%2039.5456C118.798%2044.1987%20122.233%2047.7363%20126.725%2047.7363C128.574%2047.7363%20130.262%2047.1346%20131.583%2046.0776C131.216%2048.3528%20129.235%2049.8501%20126.989%2049.8501C125.609%2049.8501%20124.141%2049.2923%20123.554%2047.7363H119.326C120.251%2050.9805%20123.187%2053.0208%20126.725%2053.0208C131.642%2053.0208%20135.18%2049.7474%20135.18%2044.8299V31.6189H131.642V33.0427ZM126.989%2044.2869C124.346%2044.2869%20122.336%2042.2319%20122.336%2039.5309C122.336%2036.8299%20124.346%2034.7749%20126.989%2034.7749C129.631%2034.7749%20131.642%2036.8299%20131.642%2039.5309C131.642%2042.2319%20129.631%2044.2869%20126.989%2044.2869Z'%20fill='%235082AF'/%3e%3cpath%20d='M109.226%2031.3401C104.573%2031.3401%20101.035%2034.8778%20101.035%2039.531C101.035%2044.1842%20104.573%2047.7218%20109.226%2047.7218C112.764%2047.7218%20115.597%2045.6815%20116.786%2042.775H112.661C111.809%2043.7292%20110.606%2044.287%20109.226%2044.287C107.083%2044.287%20105.365%2042.9366%20104.793%2040.9842H117.285C117.358%2040.5145%20117.417%2040.0007%20117.417%2039.531C117.417%2034.8778%20113.879%2031.3401%20109.226%2031.3401ZM104.778%2038.0778C105.365%2036.1255%20107.083%2034.775%20109.211%2034.775C111.34%2034.775%20113.072%2036.1255%20113.644%2038.0778H104.763H104.778Z'%20fill='%235082AF'/%3e%3cpath%20d='M98.6138%2026.3203H95.0762V47.4579H98.6138V26.3203Z'%20fill='%235082AF'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_2008_12343'%3e%3crect%20width='160'%20height='78.4'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

'%3e%3cg%20clip-path='url(%23clip1_1328_798)'%3e%3crect%20width='22'%20height='16'%20rx='2'%20fill='%231A47B8'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M2.34035%200H0V2.66667L19.6469%2016L22%2016V13.3333L2.34035%200Z'%20fill='white'/%3e%3cpath%20d='M0.780579%200L22%2014.4378V16H21.2377L0%201.54726V0H0.780579Z'%20fill='%23F93939'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M19.9048%200H22V2.66667C22%202.66667%208.39122%2011.5499%202.09524%2016H0V13.3333L19.9048%200Z'%20fill='white'/%3e%3cpath%20d='M22%200H21.2895L0%2014.4502V16H0.780579L22%201.55895V0Z'%20fill='%23F93939'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M8.00075%200H14.0176V4.93527H22V11.0615H14.0176V16H8.00075V11.0615H0V4.93527H8.00075V0Z'%20fill='white'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9.26316%200H12.7368V6.15385H22V9.84615H12.7368V16H9.26316V9.84615H0V6.15385H9.26316V0Z'%20fill='%23F93939'/%3e%3c/g%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_1328_798'%3e%3crect%20width='22'%20height='16'%20fill='white'/%3e%3c/clipPath%3e%3cclipPath%20id='clip1_1328_798'%3e%3crect%20width='22'%20height='16'%20rx='2'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Mergers & Acquisitions: practical and legal guide 2026

Authors: Olivier Sanviti, PhD, Attorney at the Paris and Madrid Bars, founder and Managing Partner act legal France, with the participation of Mariam Tourabaly and Linda Boudouaouir Attorneys at the Paris Bar

Date: March 2026

Subject: complete M&A Guide: Sell, Buy, Restructure your Company.

General Introduction

The mergers and acquisitions (M&A) market for SMEs and mid-caps in France experienced new momentum in 2025. After a year 2024 marked by wait-and-see attitudes, we are witnessing a recovery in transactions, driven by stabilization of interest rates and increased need for sectoral consolidation.

This guide was designed to answer, in an operational manner, the questions most frequently asked by business leaders facing these complex challenges. Whether preparing for transmission, achieving external growth, opening capital or retaining key executives, each step requires rigorous preparation and expert support.

Summary: what you will find in this guide

Target audience: SME/Mid-Cap Leaders, CEO, CFO, entrepreneurs, investors

Objective: Complete operational guide to navigating M&A transactions

Content structured in 8 chapters:

- Chap. 1-2: Sale and acquisition processes (preparation, due diligence, negotiation, closing)

- Chap. 3-4: Legal and financial instruments (shareholders' agreement, fundraising, term sheet)

- Chap. 5: Management package and executive incentives (BSPCE, AGA, LBO)

- Chap. 6: Valuation methods (EBITDA multiples, DCF, ESG premium)

- Chap. 7: Fatal errors to avoid (top 5 recurring traps)

- Chap. 8: Cross-border operations (act legal 19 countries)

Practical tools included:

- 3 downloadable checklists (seller 20 pts, buyer 25 pts, post-closing 15 pts)

- 4 explanatory diagrams (LBO structure, earn-out, waterfall, M&A timeline)

- 5 comparative tables (Share/Asset Deal, costs, multiples, European countries, LBO types)

- FAQ 15 essential questions with detailed answers

- M&A Glossary 50+ defined terms (from "Strategic Buyer" to "WACC")

- 3 concrete practical cases (Tech LBO, industrial acquisition, cross-border)

Market data 2025: ~850 transactions, 47% cross-border (+77% vs 2024), updated sector multiples, AI & ESG trends

Estimated reading time: 40-55 minutes (complete reading) | 10-15 minutes (targeted navigation by chapter)

Market Context 2025 in Figures

M&A Recovery: transaction volumes are rising again (+20% expected in US, +10% in Europe), particularly on the "Smid-Cap" segment (valuation < €500M).

Cross-border: 47% of transactions now involve a foreign counterparty (+77% vs 2024), confirming the internationalization of French SMEs/mid-caps. Major examples: Sanofi/Blueprint Medicines ($9.6bn), BPCE/Novo Banco (€5.6bn).

France SME/Mid-Cap: 6,800 Mid-Caps and 160,000 SMEs constitute a considerable pool.

New Key Factors: Artificial Intelligence (AI) is starting to transform due diligence, while ESG criteria (Environmental, Social, Governance) directly impact valuation (premium of 10-15% for top performers). Investment funds now quasi-systematically integrate ESG grids into their investment theses.

Table of Contents

- Chapter 1 : How to sell your company

- Chapter 2 : Buying a company: steps to a successful acquisition

- Chapter 3 : Shareholders' Agreement

- Chapter 4 : Fundraising

- Chapter 5 : Management package

- Chapter 6 : Understanding Company Valuation

- Chapter 7 : Errors to Avoid

- Chapter 8 : Cross-Border Operations

- Annex: Case Studies and Business Cases

- FAQ: 15 Essential Questions

- M&A Glossary: 50+ Defined Terms

- Sources

Chapter 1: How to sell your company?

Selling your company is often the culmination of a professional life. It is a major patrimonial operation that cannot be improvised. Whether the motivation is retirement, backing by a group to accelerate development, or exit of a financial investor, the key to success lies in preparation.

1. Preparation: The Crucial Step

A well-prepared company sells better and for more. Ideally, this process starts 12 to 24 months before going to market.

- Preliminary Audit (vendor due diligence): anticipate legal, tax or social weaknesses and, if necessary, proceed with their regularization before a buyer discovers them.

- Documentation: structure a complete and organized data room.

- IP Protection: verify that trademarks, domain names, patents and software belong to the company (and not to directors or providers) and are correctly protected before sharing them with potential buyers.

- Legal Clean-up: update registers, purge regulated agreements, secure key contracts and generally regularize what can be (especially in social matters: CSE election...).

AI Impact on Data Room

Using AI now allows automating document classification, anonymizing sensitive data (GDPR) and pre-analyzing contractual risks. This can accelerate data room setup by several weeks.

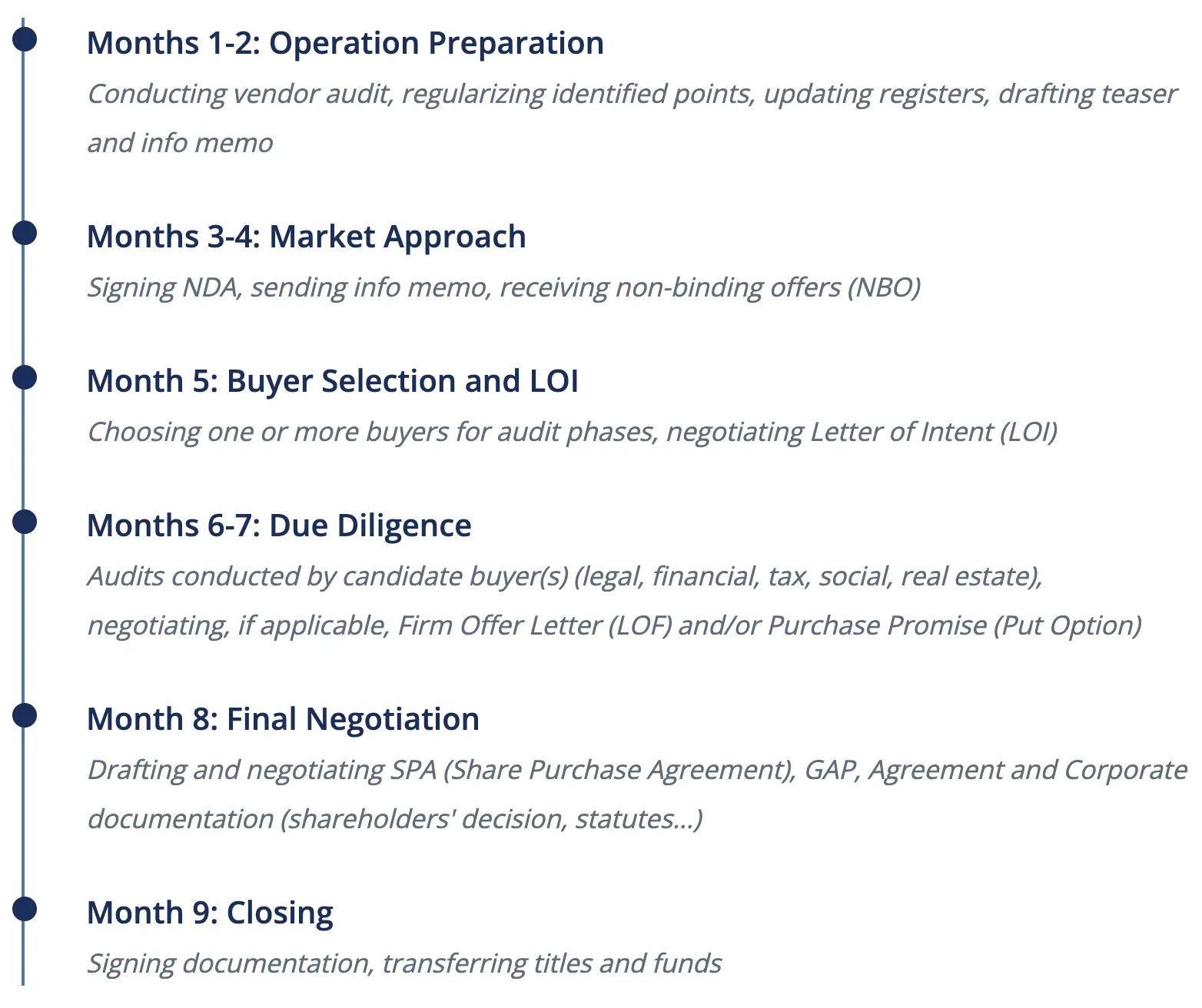

2. The Sale Process

3. Price Mechanisms and Warranties

Pricing is central, but payment terms are just as important.

- Locked Box vs Completion Accounts: the "locked box" mechanism (fixed price based on financial situation stopped before closing) is gaining ground for its simplicity, versus post-closing price adjustment ("completion accounts").

- Earn-out (price supplement): clause allowing part of the price to be paid later subject to achieving qualitative or quantitative targets (EBITDA, Revenue). Essential device in economic uncertainty.

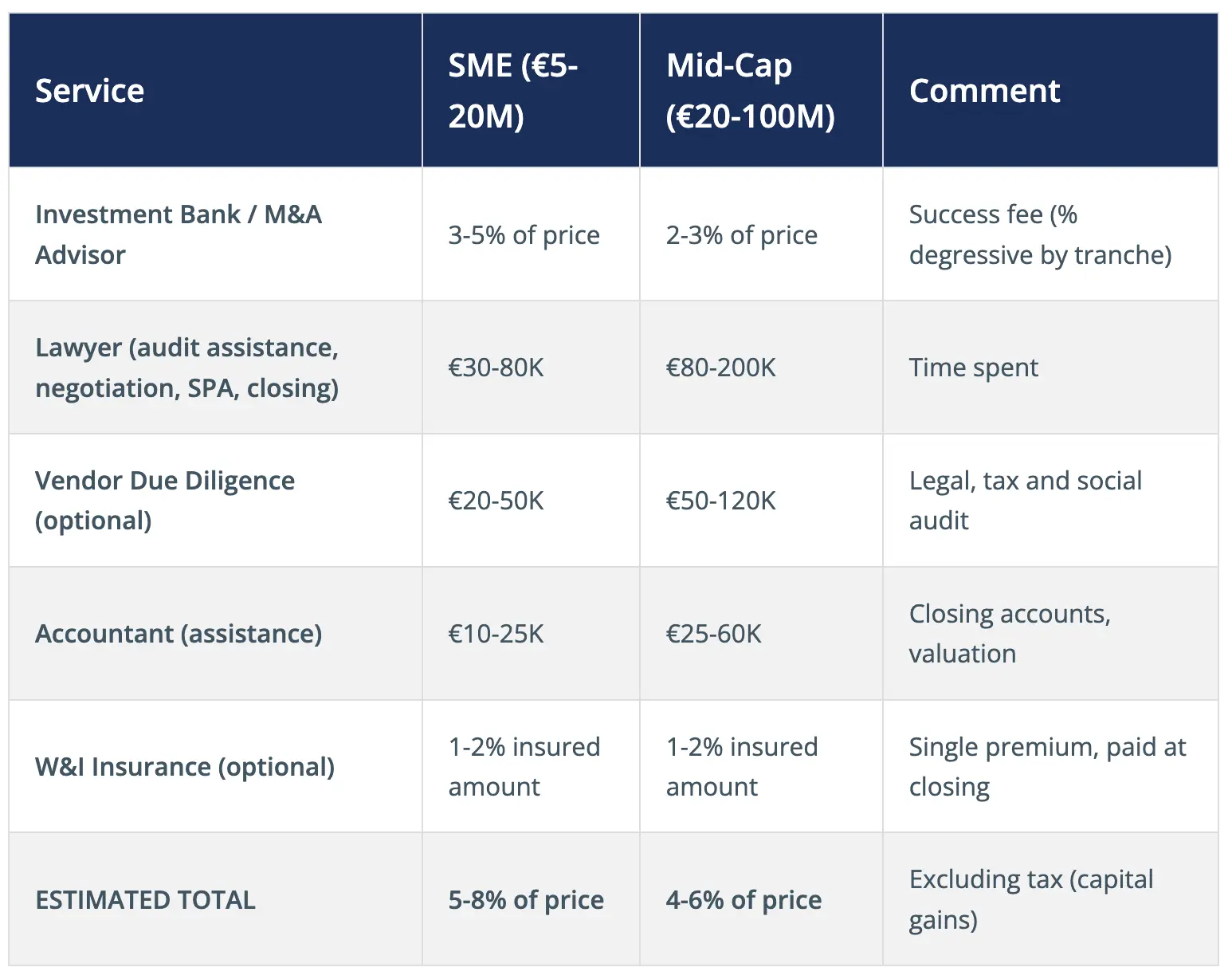

Market Context 2025 in Figures

Source: act legal France estimations, market 2025-2026. Indicative amounts, variable according to complexity.

Asset and Liability Warranty (GAP)

This is the cornerstone of buyer security. It must be carefully negotiated:

- Threshold or deductible ("basket"): minimum damage amount to trigger warranty.

- Cap: maximum amount seller agrees to pay (generally 10 to 30% of price) in case of warranty claim by buyer.

- Duration: often 18 to 24 months generally, duration of applicable limitation period for tax matters.

- Escrow: blocking part of price to guarantee potential payments under GAP. Mechanism often degressive over GAP duration.

In many transactions (especially competitive sale processes), GAP can be covered by insurance taken out with specialized insurer. This mechanism, called warranty & indemnity insurance (W&I), is widely used in mid-market transactions.

Chapter 2: Buying a company: steps to a successful acquisition

External growth is a powerful lever to gain market share, acquire technology or expand internationally. However, according to studies, nearly 50% of acquisitions fail to create expected value, often due to lack of integration or diligence.

1. Strategy and Identification

Before hunting, you must define your target. The investment thesis must be clear: cost synergies, revenue synergies, geographical or technological diversification. In 2025, Tech, Health and Energy Transition sectors were particularly prized.

Share Deal vs Asset Deal: Comparative Table

2. Valuation and Offer (LOI)

The indicative offer takes the form of a Letter of Intent (LOI). It sets the main lines: price range, scope, conditions precedent (financing, audits), exclusivity.

See Chapter 6 for valuation methods.

3. Due Diligence (Acquisition Audit)

The moment of truth. The buyer audits the target thoroughly:

- Legal: client contracts, disputes, leases, corporate, IP-IT, GDPR.

- Tax & Social: latent liabilities, URSSAF adjustment risk, VAT, litigation risks with employees...

- Financial: EBITDA quality, normative WC, net debt.

- Operational & IT: system robustness, cybersecurity.

- ESG: environmental compliance, parity, governance.

AI in Due Diligence

AI tools today allow analyzing thousands of contracts in a few hours to identify change of control clauses or atypical risks. This can reduce costs but not necessarily improve quality. Human review remains necessary in assessing risks for a buyer.

4. Negotiation and Closing

Following the audit, the buyer sends the seller a Firm Offer (LOF) specifying main proposed terms: price, warranties, schedule, financing. In case of multiple buyers, offers are negotiated and the seller retains the offer they deem best. Once LOF is countersigned, counsels for both parties negotiate and draft transaction completion documentation (SPA, GAP, shareholders' agreement if applicable).

5. Post-Acquisition Integration ("The 100 Days")

Success is determined after closing. The first 100 days integration plan is vital: communication to teams, merging IT systems, harmonizing corporate cultures, securing key personnel.

Chapter 3: Shareholders' Agreement

The shareholders' agreement is the "secret" contract (not public, unlike statutes) governing relations between shareholders. It is indispensable as soon as there are multiple shareholders, and mandatory upon entry of investors.

"The shareholders' agreement provides for capital exit scenarios."

Olivier Sanviti, Les Échos (14.10.2015)

1. Governance: Who Decides What?

The agreement organizes power beyond simple capital ownership.

- Collegial Body: creation of Strategic Committee or Supervisory Board.

- Investor Veto Right: list of decisions requiring investor approval (budget, debt, executive recruitment...).

- Enhanced Information Right: mandatory monthly or quarterly reporting.

2. Shareholding Control: Who Owns Capital?

These clauses manage share movements to ensure stability and liquidity.

3. Key Men and Women: Leaver Clauses

These clauses determine the share repurchase price of a manager in case of departure from the company.

- Bad Leaver (dismissal for fault, resignation, breach of contractual commitments...): repurchase at nominal value or with a heavy discount (sanction mechanism).

- Medium Leaver (early departure of manager without serious fault): repurchase at an intermediate value between nominal and fair market value.

- Good Leaver (death, disability, retirement, dismissal without cause): repurchase at fair market value. This is the most favourable scenario for the departing manager.

The "Bad–Medium–Good" framework is gradually disappearing, giving way to a single valuation formula applied regardless of the reason for exercising the share repurchase undertaking, incorporating a minority discount and/or an illiquidity discount.

Leaver Clauses: Recent Case Law

French courts have recently clarified the conditions under which bad leaver clauses can be applied. The definition of "fault" or "wrongful departure" must be precisely described in the shareholders' agreement to avoid disputes. Overly broad or vague definitions risk being struck down by courts as disproportionate penalties. Best practice: include a specific, exhaustive list of qualifying events rather than general language.

4. Non-Compete and Confidentiality

The shareholders' agreement typically includes non-compete and confidentiality obligations binding on managers and key shareholders.

- Non-compete clause: prohibits the departing manager from engaging in competing activities. To be valid under French law: (1) limited duration (maximum 2-3 years), (2) defined geographic scope, (3) defined sector scope, (4) justified by the company's legitimate interests. If uncompensated and excessively broad, the clause may be unenforceable.

- Confidentiality: obligation to protect trade secrets, client lists, business strategies and financial data. Generally unlimited in duration for genuine trade secrets.

5. Reserved Matters (Qualified Majority Decisions)

Investors typically negotiate a list of decisions that require their approval or a qualified majority vote, regardless of their percentage shareholding. Typical reserved matters include:

- Acquisition or disposal of assets above a defined financial threshold

- Taking on significant financial debt or granting security interests

- Material modification of the business plan or annual budget

- Hiring or dismissal of key executives (CEO, CFO, CTO)

- Creation of subsidiaries or entry into joint ventures

- Related-party transactions (agreements with shareholders or affiliates)

- Any decision to sell or merge the company

Chapter 4: Fundraising

Fundraising allows a company to accelerate its development by bringing in external capital — an alternative or complement to bank debt. It involves opening the share capital to new investors: business angels, venture capital funds, private equity, or family offices.

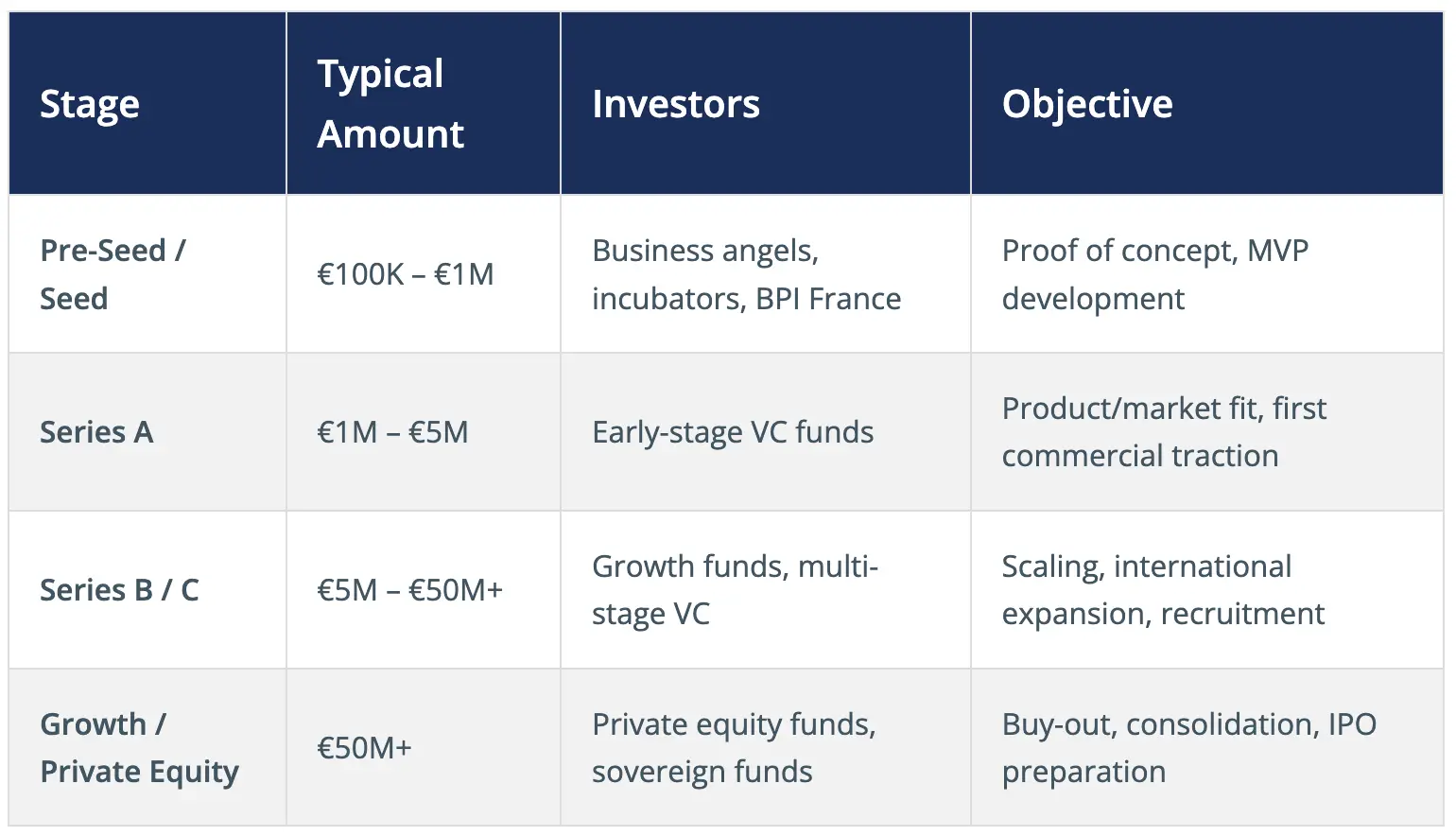

1. Types of Fundraising by Stage

2. The Term Sheet: Key Terms

The term sheet is a summary document that sets out the main conditions of fundraising before the full shareholders' agreement is drafted. It is generally non-binding (except for confidentiality and exclusivity clauses) but sets the framework for negotiations.

- Pre-money vs Post-money Valuation: the pre-money valuation is the company's value before the capital increase; the post-money valuation equals pre-money + amount raised. Example: company valued at €10M pre-money raises €2M → post-money = €12M; investor receives 16.7% of capital (€2M / €12M). Founders are diluted from 100% to 83.3%.

- Liquidation Preference Clause: protects investors in the event of a sale at a low price. A 1× non-participating liquidation preference means the investor recovers their initial investment before any distribution to founders. In a participating version ("double dip"), the investor also participates pro-rata in the remaining distribution.

- Governance of the company: organisation of decision-making power, voting rights, veto rights on reserved matters, board composition, reporting obligations, decision thresholds requiring investor approval.

- Anti-dilution (Ratchet) Clause: protects investors against down-rounds (subsequent funding rounds at a lower valuation). Two main variants: full ratchet (adjusts price to the lowest new price, very investor-friendly) and broad-based weighted average (more balanced, accounts for the number of new shares issued).

- Share Transfer (pre-emption, approval, drag-along, tag-along): conditions governing share movements: pre-emption gives existing shareholders a right of first refusal; approval clauses require consent from other shareholders; drag-along allows majority to force minority to sell; tag-along allows minority to join a majority sale on the same terms.

ESG Criteria: A New Imperative

Investment funds now virtually systematically integrate ESG (Environmental, Social, Governance) criteria into their investment thesis. Companies that do not meet ESG standards risk having difficulty raising capital or suffering a valuation discount. Conversely, strong ESG performers can command a premium of 10–15% on valuation multiples. An ESG audit (carbon footprint, gender equality index, governance structure) is increasingly required as part of investor due diligence.

3. The Fundraising Process

4. French State Aid and Public Financing

Several public mechanisms can complement or replace private investment, particularly for SMEs at early stages:

- BPI France (Banque Publique d'Investissement): direct loans, guaranteed bank loans, equity investment through BPI Capital, innovation grants.

- CIR (Research Tax Credit): up to 30% of eligible R&D expenditure, refundable for SMEs. Key tool for tech and industrial companies.

- JEI Status (Young Innovative Company): significant social security exemptions for companies investing more than 15% of turnover in R&D. Valid for the first 11 years.

- Regional & European subsidies: FEDER, FEADER, regional development grants through Regions and ADEME (environment and energy transition).

Chapter 5: Management Package

The management package is the financial incentive mechanism designed to align the interests of managers and executives with those of financial shareholders (PE funds, investors). It is used systematically in PE and LBO transactions, and increasingly in fundraising rounds.

1. Main Instruments

- Free Shares (AGA – Actions Gratuites): shares awarded free of charge to employees or executives, subject to a minimum vesting period of 1 year and a holding period of 1 year.

- BSPCE (Business Creator Share Subscription Warrants): warrants reserved exclusively for innovative companies. Very favourable tax regime and no employer social security charges. The most popular instrument in French startups.

- Preference Shares (ADP – Actions de Préférence): shares with specific financial rights distinct from those of ordinary shares (e.g., super-dividend triggered on performance, priority in distributions, or accelerated vesting). These instruments can apply to ordinary or preference shares that have financial rights distinct from those of other shareholders.

2026 Tax Reform – Management Package (Art. 163 bis H CGI)

Following a landmark Council of State ruling in 2021, the management package taxation framework was overhauled. Key points:

- Flat tax qualification (31,40%): applies when the beneficiary bears a real capital risk (invested personal funds at risk).

- Cap mechanism: beyond a 3× project multiple gain (i.e., gain exceeds 3 times the initial investment), the surplus may be reclassified as salary income and taxed at the marginal income tax rate (up to 59% including social levies).

- Practical implication: management package structures must be carefully designed with tax counsel to ensure the capital-risk condition is genuinely met and documented.

- Escrow: blocking part of price to guarantee potential payments under GAP. Mechanism often degressive over GAP duration.

2. LBO Structuring

Management company structures (ManCo), historically frequent in LBOs, tend to be used with greater caution due to risks of tax reclassification.

Investors now favour more direct and secure schemes, based on personal investment by executives.

Management company structures (ManCo), historically frequent in LBOs, tend to be used with greater caution today due to risks of tax reclassification. Investors now prefer more direct and secure schemes based on personal investment by executives.

Chapter 6: Understanding Company Valuation

Valuation is not an exact science but an argued financial opinion. Several methods coexist and complement each other; the choice depends on the company's profile, sector, and stage of development.

1. EBITDA Multiples Method (Most Common in SME M&A)

The most widely used method for SMEs and mid-caps. The formula is simple: Enterprise Value = EBITDA × Multiple. The multiple reflects sector attractiveness, growth profile, margin quality and market conditions.

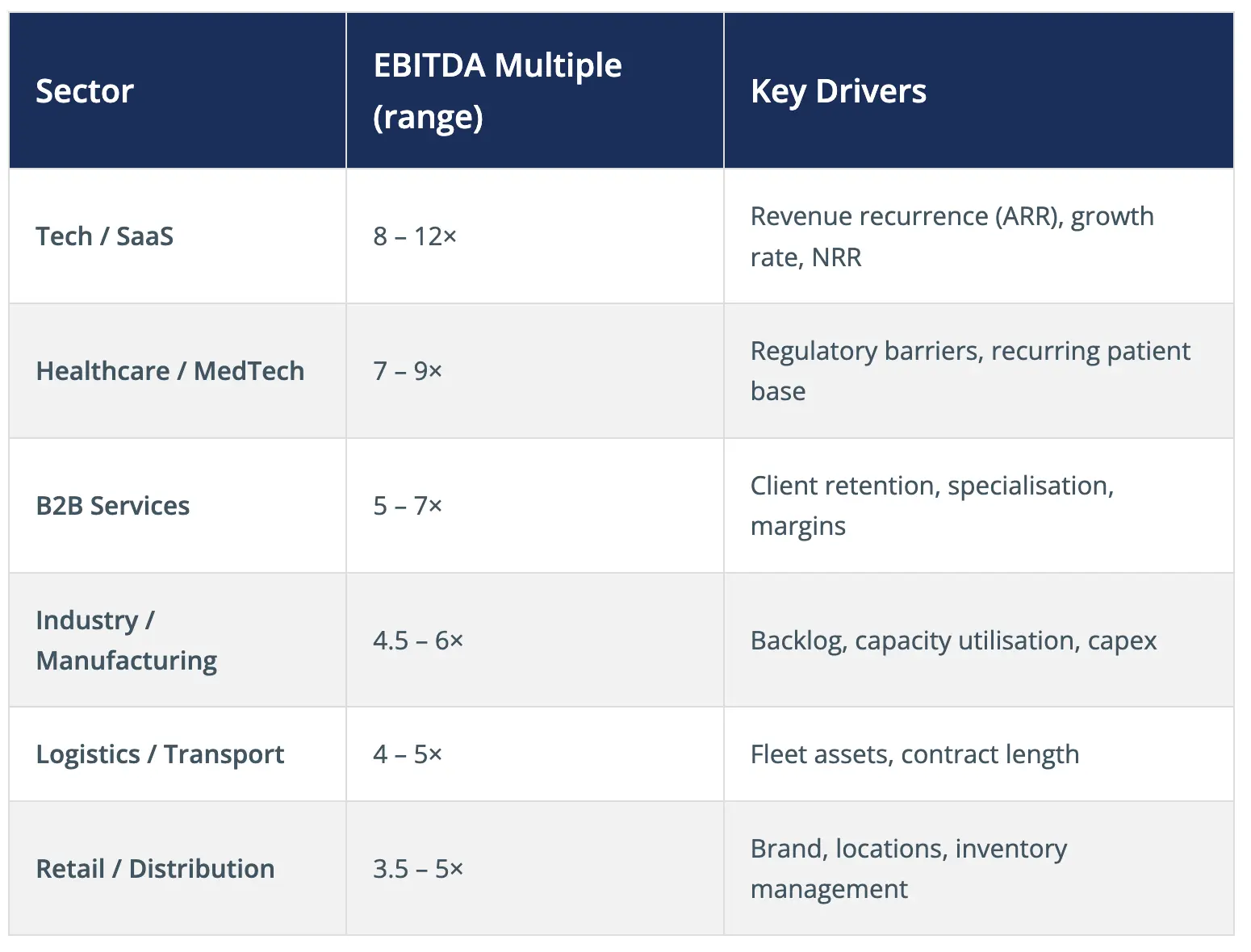

Sector EBITDA Multiples – France 2026

Source: Argos Index, Capital IQ, act legal France estimates – market 2025-2026. Indicative ranges.

ESG Premium on Valuation

Companies with a strong ESG profile (low carbon footprint, high gender equality index, robust governance) can command a valuation premium of 10–15% versus sector peers. Conversely, companies with significant ESG risks (environmental non-compliance, poor governance, no CSR policy) face valuation discounts and increasing difficulty attracting institutional investors.

2. DCF Method (Discounted Cash Flows)

The DCF method values a company by discounting projected future free cash flows at the weighted average cost of capital (WACC). More theoretically rigorous but highly sensitive to assumptions.

- Forecast period: 5 to 7 years of explicit cash flow projections.

- Terminal value: value beyond the forecast period, calculated using a terminal growth rate (typically 1.5–2.5% for mature businesses).

- WACC: typically 8–12% depending on risk profile, capital structure and sector.

- Use case: mainly used for large transactions, leveraged finance models, or specific asset valuations.

3. Asset-Based / Patrimonial Method

The Net Asset Value (NAV) method values a company by revaluing its assets and liabilities at fair market value. NAV = Total assets (at fair value) – Total liabilities. Used primarily for:

- Holding companies and real estate investment companies

- Companies with significant tangible assets (industrial, agricultural)

- Distressed situations or liquidation scenarios

4. Transaction Comparables

Analysis of recent comparable transactions in the same sector provides market-based evidence for valuation. Key sources: Capital IQ, Mergermarket, Argos Index (the French mid-market benchmark published quarterly). This method complements multiple analysis and is particularly useful for validating offer prices in competitive sale processes.

5. From Enterprise Value to Equity Value

The purchase price paid to shareholders (Equity Value) differs from the Enterprise Value:

- Equity Value = Enterprise Value – Net Financial Debt + Surplus Cash

- Working Capital adjustment: if the actual working capital at closing differs from the normative (reference) working capital agreed at signing, the price is adjusted up or down accordingly.

- Earn-out: bridges the valuation gap between seller's and buyer's expectations by tying a portion of the price to post-closing performance.

Chapter 7: Fatal Errors to Avoid

Based on act legal France's experience advising on hundreds of transactions, five recurring traps consistently account for failed or value-destroying M&A deals. Awareness is the first step to avoidance.

Error 1: Insufficient Preparation

The trap: launching a sale process without prior preparation, no vendor due diligence, a disorganised data room, missing corporate documents, unresolved disputes or unregistered IP.

Consequence: buyer discovers issues during due diligence → requests price reduction, conditions or abandons the process entirely. Process interrupted at the most advanced stage.

Solution: start preparation 12 to 24 months before going to market. Conduct a VDD, clean up the corporate structure, regularise social/tax situation, register trademarks and domain names.

Error 2: Neglecting Due Diligence

The trap: buyers who skip or rush due diligence to save time or reduce costs, relying on management representations without independent verification.

Consequence: post-closing discovery of hidden liabilities (tax adjustments, undisclosed debt, labour disputes, environmental issues).

Solution: invest in comprehensive due diligence with specialised advisors (legal, financial, tax, IT, ESG). The cost (€30–150K) is negligible compared to the risks avoided.

Error 3: Poorly Drafted Shareholders' Agreement

The trap: using a standard template without customisation — missing clauses (no drag-along, ambiguous leaver definitions, no deadlock mechanism), or overly complex provisions that paralyse decision-making.

Consequence: governance crises, minority shareholder blockages, difficulty exiting the investment, prolonged and costly disputes.

Solution: engage an experienced M&A lawyer to tailor clauses to the specific situation. Scenario-test each clause: what happens in a deadlock? What is the exit mechanism?

Error 4: Underestimating Integration Challenges

The trap: no integration plan prepared before closing, poor communication to teams, key person departures, IT system incompatibilities ignored.

Consequence: value destruction in the first year, client departures, talent loss, cultural clash leading to demotivation. Studies show that 50% of acquisitions fail to create expected value, primarily due to integration failures.

Solution: prepare the integration plan from the signing date. Appoint a dedicated integration manager. Communicate early and transparently to all stakeholders.

Error 5: Tax and Structuring Errors

The trap: wrong holding structure, forgetting earn-out tax implications, poorly structured management package, ignoring international tax issues in cross-border deals.

Consequence: unexpected tax bill reducing transaction economics by 5–20% of deal value. Reclassification of capital gains as salary income. Permanent establishment risks in cross-border transactions.

Solution: involve a tax advisor from the very beginning of the transaction structuring phase, not at the last minute before signing.

Checklist: 5 Questions to Ask Before Signing

- Have I conducted a Vendor Due Diligence (VDD) and corrected identified weaknesses?

- Is my data room complete, organised and tested with a third party?

- Have I stress-tested all earn-out and price adjustment clauses with my lawyer?

- Has a tax advisor reviewed the acquisition/sale structure?

- Is my 100-day integration plan ready and assigned to a named owner?

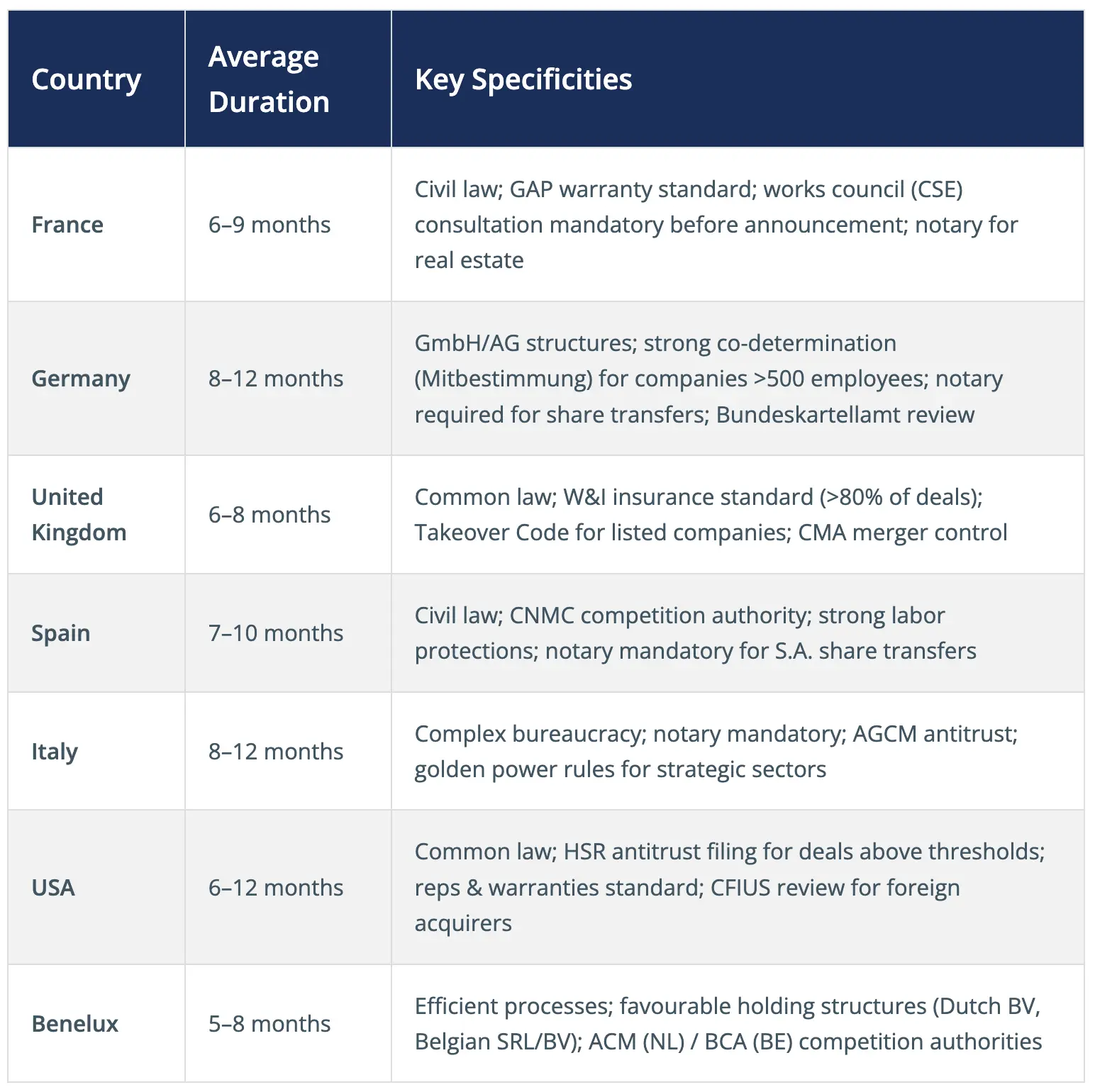

Chapter 8: Cross-Border Operations

In 2025, 47% of French SME and mid-cap M&A transactions involved a foreign counterparty (+77% vs 2024), confirming the accelerating internationalisation of French businesses. The act legal network spans 19 European countries, providing integrated local expertise for cross-border deals.

1. Key Specificities of Cross-Border M&A

- Applicable law: which country's law governs the SPA? This is a critical negotiation point. Choice of law affects warranty interpretation, limitation periods and dispute resolution.

- Multi-jurisdictional regulatory approvals: merger control filings may be required in multiple jurisdictions (France ADLC, European Commission, Germany Bundeskartellamt, USA DOJ/FTC). Timeline and thresholds vary significantly.

- Currency risk: for deals with a foreign currency component, consider hedging instruments (forward contracts, options) to protect against exchange rate movements between signing and closing.

- Cultural negotiation differences: US/UK style (fast, adversarial, W&I insurance standard), French/German style (relationship-based, notarial formalities in Germany), Asian style (longer relationship building, face-saving important).

- International tax structuring: double tax treaty analysis, permanent establishment risks, transfer pricing rules for intra-group transactions, withholding taxes on dividends and interest.

2. Comparative M&A Process by Country

Foreign Investment Control

Cross-border investments in sensitive sectors require specific regulatory filings:

- France (IFR – Investissement Étranger en France): prior authorisation required from the Ministry of Economy for investments by non-EU investors in strategic sectors: defence, health, telecoms, media, energy, AI, semiconductors. Threshold: acquisition of >25% voting rights (or control). Review period: 30 working days (extendable).

- European Union: new FDI (Foreign Direct Investment) screening regulation imposes cooperation between EU Member States; no single EU approval but coordinated assessment for strategic investments.

3. The act legal continental European coverage

act legal operates across 19 European countries with local teams offering integrated M&A advice: France, Austria, Belgium, Bulgaria, Czechia, Germany, Hungary, Italy, Netherlands, Poland, Romania, Slovakia, Spain, Western Balkans. The pan-European model ensures consistent deal management with genuine local expertise in each jurisdiction.

4. Practical Tips for Cross-Border Deals

- Appoint a lead counsel with proven international M&A coordination experience from day one.

- Budget specifically for certified translation costs (required for official filings and notarial deeds).

- Allow additional time for regulatory filings: add 2–4 months to standard timelines for multi-jurisdictional deals.

- Understand and comply with local labour consultation requirements before any public announcement.

- Verify foreign investment control filing obligations early, failure to file can result in nullity of the transaction.

Annex: Case Studies and Business Cases

Case Study 1: Tech LBO - SaaS Company

Situation: A French B2B SaaS company, €15M revenue (90% recurring ARR), 25% EBITDA margin (€3.75M EBITDA), strong growth trajectory (+30% YoY).

Valuation: Enterprise Value = €3.75M × 8 = €30M. Net debt: zero. Equity Value: €30M.

LBO Structure: NewCo borrows €21M (senior debt, 70%), PE fund provides €7M equity (23%), management team co-invests €2M (7%). Management receives BSPCE warrants on 10% fully diluted, exercisable on exit at a return hurdle of 2×.

Earn-out: additional €3M payable if ARR exceeds €20M at end of Year 2 post-closing.

Key Issues Addressed: BSPCE tax qualification (capital risk condition met), change-of-control clauses in 2 major client contracts (waiver obtained pre-closing), data room GDPR compliance (DPO appointed, processing register updated).

Case Study 2: Industrial Strategic Acquisition (France - Germany)

Situation: A French industrial manufacturer (€60M revenue, €8M EBITDA) acquires a German competitor (€30M revenue, €5.5M EBITDA) for €45M (5.5× blended EBITDA). Rationale: geographic expansion, production capacity, technology acquisition.

Structure: Share Deal chosen to preserve continuity of German client contracts. SPA governed by French law with German notarial deed for share transfer.

Key Challenges: German works council (Betriebsrat) consultation process required 2 months before announcement. Three major client contracts contained change-of-control clauses requiring counter-party consent. GDPR cross-border data transfer mapping required.

Integration: 100-day integration roadmap prepared before closing. IT systems merger completed in 6 months. Two senior German executives retained with 3-year lock-up and management package.

Case Study 3: Cross-Border Deal - France / Spain

Situation: A French B2B services company (€20M revenue) acquired by a Spanish PE fund for €28M (7× EBITDA). The fund is closing its second fund targeting South European services companies.

Regulatory: Spanish CNMC merger control notification assessed, below thresholds, no filing required. French IFR screening: non-EU acquirer (fund domiciled in Luxembourg) → filing made, authorisation received within 30 days (no sensitive sector involvement).

Legal Structure: SPA governed by French law. Works council (CSE) consulted. W&I insurance taken out.

Result: Transaction closed in 8 months from mandate to closing. Seller received full €28M at closing (no earn-out), with 18-month non-compete. Management team retained with 15% equity stake in the acquiring NewCo.

FAQ: 15 Essential Questions

1. What is the difference between an LOI and a SPA?

The LOI (Letter of Intent) is a preliminary, generally non-binding agreement that sets out the main terms of the transaction: indicative price range, key conditions, exclusivity period and confidentiality obligations. The SPA (Share Purchase Agreement) is the definitive, legally binding sales contract, containing all representations, warranties, conditions precedent and price mechanisms.

2. How long does a company sale take?

On average, allow between 6 and 12 months between the formal decision to sell and the closing (final signature and fund transfer). Preparation (VDD, data room) typically requires an additional 2–6 months beforehand. Cross-border transactions or those requiring regulatory approvals can take longer.

3. What is a Bad Leaver clause?

A Bad Leaver clause in a shareholders' agreement stipulates that a manager leaving the company for a wrongful reason (dismissal for fault, early resignation, breach of obligations) must sell back their shares at a discounted price (often at nominal value). It is a sanction mechanism designed to incentivise managers to stay and perform. Its counterpart, the Good Leaver clause, provides fair market value repurchase for justified departures (retirement, death, disability, dismissal without cause).

4. Why conduct a Vendor Due Diligence (VDD)?

A VDD allows the seller to identify and correct weaknesses upstream, before a buyer discovers them (which would result in a price reduction or deal failure). Benefits: (1) reassure buyers and accelerate the process, (2) demonstrate transparency and professionalism, (3) often obtain a better price by removing uncertainty, (4) prepare management for buyer Q&A.

5. How does the Earn-out mechanism work?

An earn-out is a conditional price supplement paid to the seller after closing, if the company achieves defined performance targets (Revenue, EBITDA, ARR) over an agreed period (typically 1 to 3 years). It bridges the valuation gap between seller's optimistic projections and buyer's conservative estimates. Key negotiation points: choice of metric, measurement period, how the metric is defined (accounting vs commercial), and governance of the company during the earn-out period.

6. What is the difference between a Share Deal and an Asset Deal?

A Share Deal consists of acquiring the company's shares/units. The buyer takes over the legal entity with ALL its assets AND liabilities (contracts, debts, disputes, history). Tax-wise, this is more favourable to the seller (capital gains at 31.4% flat tax for individuals). An Asset Deal consists of buying only selected assets (goodwill, patents, equipment, client lists) without taking over the legal entity or historical liabilities. The buyer chooses exactly what they acquire. Tax-wise, more favourable to the buyer (assets can be depreciated).

7. How to calculate net debt in an acquisition?

Net Debt = Gross Financial Debt − Cash − Cash Equivalents. Gross debt includes: bank loans, bonds, overdrafts, shareholders' current accounts (debt position), lease liabilities (IFRS 16), guarantees and certain off-balance sheet commitments. Net debt is a key valuation bridge element: Enterprise Value (EV) = Equity Value + Net Debt. A higher net debt reduces the equity value (and therefore the price paid to shareholders) for the same EV.

8. What is a MAC (Material Adverse Change) clause?

A MAC clause is a contractual condition precedent allowing the buyer to withdraw from or renegotiate the transaction if a serious event significantly and adversely affects the target between the signing of the LOI/SPA and the closing. Examples: loss of a major client, natural disaster, major regulatory change, pandemic. In practice, MAC clauses are extremely difficult to invoke successfully — courts and arbitration tribunals set a very high threshold for what constitutes a "material" adverse change.

9. When is authorisation from the Competition Authority required?

France (ADLC): notification mandatory if (1) combined worldwide turnover >€150M AND (2) at least two parties have French turnover >€50M. European Commission: combined worldwide turnover >€5bn AND European turnover of each of at least two parties >€250M. Review periods: 25 working days (Phase 1) or up to 90 working days (Phase 2). Failure to notify before closing can result in fines and transaction nullity.

10. How does a liquidation preference work?

A liquidation preference protects investors in case of a low-price exit. Example: an investor puts in €5M for 30% of capital (1× non-participating liquidation preference). If the company is sold for €8M, the investor first recovers their €5M investment, and the remaining €3M goes entirely to the founders. If the sale price were €20M, the investor would receive €5M (their preference) and then 30% of the remaining €15M = €4.5M, for a total of €9.5M — but only if the liquidation preference converts to participating equity above a defined threshold.

11. What is a sector valuation multiple?

A sector valuation multiple is a coefficient applied to EBITDA (or revenue for high-growth companies) to value a company by comparison with its sector. Examples 2026 France: Tech/SaaS (8–12× EBITDA), Healthcare (7–9×), B2B Services (5–7×), Industry (4.5–6×), Logistics (4–5×). Multiples vary according to company size, growth rate, revenue recurrence, margins and the availability of comparable transactions. Source: Argos Index, Capital IQ.

12. How much does a legal due diligence cost?

For an SME (valuation €5–20M): €15,000 to €50,000 excl. VAT for legal DD. For a mid-cap (€20–100M): €40,000 to €150,000 excl. VAT. Total DD cost (legal + financial + tax) typically represents 0.5–2% of transaction value. Costs vary depending on complexity, number of jurisdictions, scope, deadlines and quality of data room organisation.

13. Can an acquisition be cancelled after closing?

Very rarely. Once closing is completed, cancellation requires proving a defect in consent (fraud, substantial error, duress) or a seriously violated asset and liability warranty. In practice, the remedy is financial compensation via the GAP mechanism, not cancellation of the transaction. Action for nullity: 5-year limitation period under French law. Courts are very reluctant to unwind completed transactions.

14. What is Warranty & Indemnity (W&I) Insurance?

W&I Insurance is taken out by the buyer (or sometimes the seller) to cover risks linked to breach of representations and warranties in the SPA, transferring liability to an insurer. Cost: 1–2% of the insured amount, paid as a single premium at closing. Advantages: facilitates negotiation (seller can be "clean" of liability), protects buyer against insolvency of seller, avoids post-closing disputes, enables full price payment at closing. Used in approximately 40% of mid-market transactions (€20–100M) in France.

15. How to structure an LBO to buy out a company?

An LBO consists of buying a company using debt leverage: (1) creation of a takeover holding company (NewCo), (2) NewCo borrows 60–70% of the acquisition price (senior bank debt), (3) equity 20–30% provided by a PE fund and management team, (4) NewCo acquires 100% of target shares, (5) the operating company (OpCo) distributes dividends to repay debt over 5–7 years. Tax advantage: interest on acquisition debt is generally deductible. Management typically participates through BSPCE, AGA or preference shares to align their financial interests with those of the fund.

M&A Glossary: 50+ Defined Terms

AGA (Actions Gratuites – Free Shares)

Free shares awarded to employees/executives. Minimum 1-year vesting, 1-year holding. Tax: acquisition gain as salary; capital gain on disposal at flat tax. Employer social charges apply.

ARR / MRR

Annual Recurring Revenue / Monthly Recurring Revenue. Key metric for SaaS and subscription businesses. High ARR with low churn significantly increases valuation multiples.

Asset Deal

Selective acquisition of assets (goodwill, patents, equipment) without the legal entity or historical liabilities. Tax-favourable for the buyer (asset depreciation possible).

BSPCE (Bons de Souscription de Parts de Créateur d'Entreprise)

Business creator share subscription warrants. Favourable tax regime (capital gain taxed at 12.8% + 17.2% PS); no employer social charges. Reserved for companies less than 15 years old. Very popular in French startups.

Cap Table

Table showing the ownership structure of a company: who owns what percentage, which instruments are outstanding (shares, warrants, options), and the fully diluted ownership percentages.

Closing

Final step of an M&A transaction: simultaneous signing of all documents, transfer of shares and payment of the price. After closing, the transaction is legally complete.

Completion Accounts

Price mechanism where the final purchase price is adjusted after closing based on actual financial position at closing date (net debt, working capital). More complex but protects both parties against interim changes.

Cross-border M&A

Transnational transaction involving entities from different countries. Specificities: applicable law, international tax, multiple regulatory approvals, cultural negotiation differences. 47% of French deals in 2025.

Data Room / Virtual Data Room

Secure repository (physical or virtual) containing all documents shared with potential buyers during due diligence. Good data room organisation is a key indicator of seller professionalism.

DPO (Data Protection Officer)

Person responsible for GDPR compliance within an organisation. Mandatory for public authorities, companies processing data at large scale, or companies processing sensitive data.

Drag Along

Clause obliging minority shareholders to sell their shares if the majority finds a buyer for 100% of the company on the same terms. Ensures the majority can deliver full ownership to a buyer.

Due Diligence

In-depth investigation of the target (legal, financial, tax, social, IT, ESG) by the buyer before signing the SPA. Duration: typically 4 to 8 weeks.

Earn-out

Conditional price supplement paid to the seller post-closing if the company achieves defined performance targets (Revenue, EBITDA). Typical period: 1–3 years.

Earn-out

Enterprise Value (EV)

Total company value, independent of capital structure: EV = Market Capitalisation + Net Debt (or EV = EBITDA × Multiple). Reflects the value of the entire business before allocation between debt and equity holders.

Equity Value

Value attributable to shareholders: Equity Value = Enterprise Value − Net Financial Debt + Surplus Cash. This is the price paid to existing shareholders in a Share Deal.

ESG (Environmental, Social, Governance)

Framework for evaluating non-financial performance. ESG criteria are now integral to PE investment theses. Strong ESG profile can command a 10–15% valuation premium.

Financial Buyer (PE Fund) Prvate equity fund acquiring a company purely for financial return (IRR/MoM), typically over a 4–7 year hold period. Uses LBO structures and manages portfolio companies actively to create value.

GAP (Garantie d'Actif et de Passif – Asset and Liability Warranty)

Clause in the SPA by which the seller guarantees the legal, tax and social situation of the sold company. If undisclosed liabilities are subsequently discovered, the buyer can claim compensation. Typical duration: 18–24 months.

Good Leaver / Bad Leaver

Clauses defining share repurchase price for a departing manager. Good Leaver (retirement, death, dismissal without cause): fair market value. Bad Leaver (fault, resignation, breach): nominal value or heavy discount.

IRR (Internal Rate of Return)

Annualised return on investment. Primary metric used by PE funds to evaluate investment performance. Typical target IRR for mid-market PE: 20–25% per annum over a 5-year hold.

LBO (Leveraged Buy-Out)

Leveraged company buyout using significant debt (60–70% of price). A NewCo is created to borrow and acquire the target, repaying debt over 5–7 years from operating company dividends.

Liquidation Preference

Mechanism protecting investors in low-price exits: investors recover their initial investment (1×) before any distribution to founders. Variants: participating (double dip) vs non-participating.

Lock-up (Inalienability)

Contractual prohibition on selling shares for a defined period (typically 2–5 years). Ensures continuity of management commitment post-transaction.

Locked Box

Price mechanism where the purchase price is fixed based on an agreed historical balance sheet (the "locked box date"). No post-closing price adjustment. Simpler and increasingly preferred in competitive processes.

LOI (Letter of Intent)

Pre-contractual document setting out the main lines of a transaction (price, conditions, exclusivity). Generally non-binding except for confidentiality and exclusivity clauses.

M&A (Mergers & Acquisitions)

Set of transactions involving company combinations: acquisition of shares or assets, legal mergers, partial asset contributions. Also covers fundraising and LBOs.

MAC Clause (Material Adverse Change)

Condition precedent allowing buyer to withdraw if a serious event significantly affects the target between signing and closing. In practice, very difficult to invoke.

Management Package

Financial incentive scheme aligning managers' interests with shareholders'. Instruments: BSPCE, AGA (Free Shares), ADP (Preference Shares), BSA. Common in PE-backed transactions.

ManCo (Management Company)

Holding company used by managers to invest alongside a PE fund in an LBO. Its use has become less common due to tax reclassification risks identified by French tax authorities.

MBO (Management Buy-Out)

LBO variant in which the existing management team (majority or 50/50 with a fund) buys out the company. Common in family business succession and founder retirement situations.

Mezzanine Debt

Hybrid financing instrument ranked between senior debt and equity. Higher return than senior debt (10–15% vs 5–7%) but subordinated in repayment priority. Often includes warrants (equity kicker).

Multiple of Money (MoM / MOIC)

Total value returned divided by total invested capital. Complementary to IRR: a 2× MoM over 3 years has a much higher IRR than a 2× MoM over 7 years.

NBO (Non-Binding Offer)

Indicative, non-binding offer submitted by a potential buyer at the start of a sale process, setting out a price range and key conditions. Also called an IOI (Indication of Interest).

NDA (Non-Disclosure Agreement)

Confidentiality agreement signed before sharing sensitive information with potential buyers or investors. Sets out the scope, duration and penalties for breach of confidentiality.

Net Debt

Gross financial debt (bank loans, bonds, overdrafts, shareholder current accounts) minus cash and cash equivalents. Key bridge from Enterprise Value to Equity Value.

NewCo

Newly created acquisition vehicle (holding company) used in LBO transactions to borrow acquisition finance and acquire 100% of the target company (OpCo).

OpCo

Operating company: the target company that generates the cash flows used to repay the LBO acquisition debt held by NewCo.

Pre-emption

Priority right for existing shareholders to acquire shares of a selling shareholder before they are offered to third parties. Protects the stability of the shareholder base.

Ratchet (Anti-dilution Clause)

Mechanism protecting investors against down-rounds. Full ratchet: adjusts investor's price to the lowest new round price. Broad-based weighted average: more balanced, accounts for the number of new shares issued.

Senior Debt

Primary bank financing in an LBO, representing 60–70% of acquisition price. First priority in repayment. Secured against the assets and cash flows of the OpCo.

Share Deal

Acquisition of shares/units. The buyer acquires the legal entity with all its assets AND liabilities. Tax-favourable for the seller (capital gains tax at ~31.4% flat tax for individuals).

Shareholders' Agreement (Pacte d'Actionnaires)

Extra-statutory contract governing relations between shareholders. Typical clauses: pre-emption, approval, lock-up, tag-along, drag-along, liquidation preference, leaver provisions.

Signing

Execution of the SPA and related documents. In complex transactions, signing and closing may be separated by weeks or months to allow for fulfilment of conditions precedent (regulatory approvals, financing).

SPA (Share Purchase Agreement)

Definitive and legally binding share transfer contract. Contains price, representations and warranties, conditions precedent and price supplement clauses.

Strategic Buyer

Industrial or commercial acquirer (as opposed to a financial buyer/PE fund). Typically pays a higher price due to synergies (cost savings, cross-selling, market access) but requires longer integration planning.

Tag Along

Right for minority shareholders to sell their shares on the same terms and conditions if the majority shareholder sells. Protects minorities from being left with an unwanted new majority shareholder.

Term Sheet

Summary document setting main conditions of fundraising (valuation, amount, investor rights) before drafting the full shareholders' agreement.

VDD (Vendor Due Diligence)

Pre-sale audit commissioned by the seller to identify and correct weaknesses before the buyer's due diligence. Accelerates the process and often improves sale price.

W&I Insurance (Warranty & Indemnity)

Insurance transferring GAP/representations risk to an insurer. Cost: 1–2% of insured amount. Used in ~40% of mid-market transactions (€20–100M) in France.

WACC (Weighted Average Cost of Capital)Discount rate used in DCF valuation, re<br><br>flecting the weighted cost of equity and debt.

Working Capital (BFR – Besoin en Fonds de Roulement)